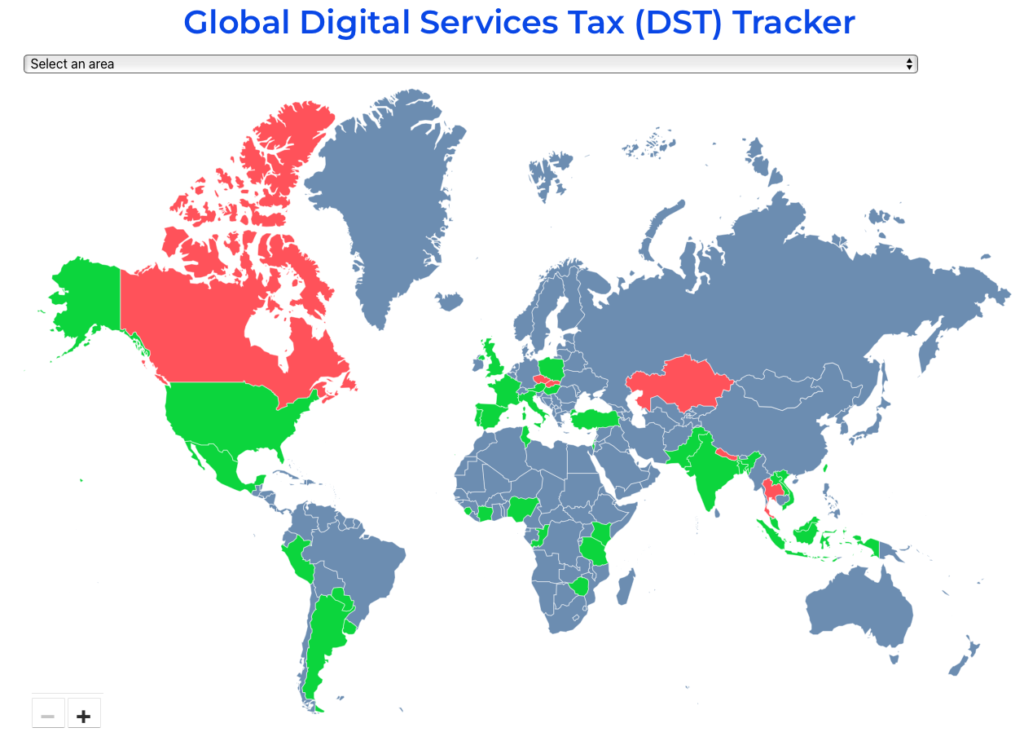

Trending Now

On November 26, 2025, Montenegro issued a Draft Law to apply a domestic minimum top-up tax (DMTT) from January 1, 2026.

On December 1, 2025, Turkey announced an extension in the filing and payment date for the QDMTT return and the opening of a test environment

On November 26, 2025, the Swiss Federal Council issued an amendment to the Minimum Tax Ordinance to provide for the OECD GIR provisions, as well

On November 19, 2025, Hungary enacted Pillar 2 amendments from the 2025 Autumn Tax Package. This includes some amendments to the operation of the Transitional

On November 14, 2025, Hungary issued a Draft Regulation (for consultation) to provide for the detailed application of the Pillar 2 Safe Harbours.

Italy has issued 2 regulations relating to the Administration of the Pillar 2 top-up tax. A November 7, 2025 Decree provides for more information on

On November 3, 2025, Finland issued a draft law for consultation to amend its Minimum Tax Act for the June 2024 and January 2025 OECD

A Communique of October 29, 2025 issued by the MRA provides further information on QDMTT Notifications.

On November 3, 2025, Kenya issued the Draft Income Tax (Minimum Top Up Tax) Regulations, 2025 to provide for the detailed application of the Pillar

")